Barbados Stock Exchange

Image credit: Unsplash

Image credit: UnsplashIntroduction

I have a vested interest in finding interesting datasets related to Barbados as that’s where I’m from.

One site which caught my interest is the Barbados Stock Exchange.

Now I’m currently ignorant when it comes to all things stocks, but I do see they offer on their website the ability to download monthly reports, and I do understand ‘free to download’.

Downloading Files

The first thing we need to do is load the information into our tool of choice, yet they’re quite a few files we’d need to download and edit.

Here we can take advantage of some automation to help us out, my tool of choice for this will be R.

We’ll first load our libraries and start writing our code.

library(conflicted)

library(tidyverse)

conflict_prefer("filter", "dplyr")

library(clock)

library(gt)Prep Work

First we download and look at some of the files manually. We thus confirm that we can download the reports as csv files from the link, > [Domain]/reports/monthly/download-csv?tradeDate=[Date] > >where [Date] is the the date of interest in the format of yyyy-mm-dd.

We can generate a sequence of dates using seq and clock which we can paste unto our base link.

This will give us a list of links for all the files we’re interested in.

# Download the data from the base link

base_link <- "https://bse.com.bb/reports/monthly/download-csv?tradeDate="

# Specify dates of interest

from <- clock::year_month_day(1910, 1)

to <- clock::year_month_day(2022, 1)

# Generate download links

download_links <- tibble::tibble(

link = paste0(base_link,

seq(from, to, by = 1),

"-01")

)We can confirm that the links were created as expected by looking at a few with the following code.

# Show some of our generated links

download_links %>%

head() %>%

gt::gt(rowname_col = NULL) %>%

gt::tab_header(

title = "List of generated links"

)| List of generated links |

|---|

| link |

| https://bse.com.bb/reports/monthly/download-csv?tradeDate=1910-01-01 |

| https://bse.com.bb/reports/monthly/download-csv?tradeDate=1910-02-01 |

| https://bse.com.bb/reports/monthly/download-csv?tradeDate=1910-03-01 |

| https://bse.com.bb/reports/monthly/download-csv?tradeDate=1910-04-01 |

| https://bse.com.bb/reports/monthly/download-csv?tradeDate=1910-05-01 |

| https://bse.com.bb/reports/monthly/download-csv?tradeDate=1910-06-01 |

Downloading Files

In our prep work, we created 1345 links to now download our files. That’s a bit, but thankfully we’re not doing this by hand, instead we’ll also be leveraging R here as well.

We’ll first create a folder called “Stock_Files” to store our downloaded files to, as I may rerun this script multiple times, I’ll only download the files if this folder doesn’t exist.

We’re also not particularly interested in any one file, so we’ll just assign them temporary names.

# Note how many files we're interested in

val <- nrow(download_links)

# If I've downloaded the files already, just use them, otherwise download them

if( length( list.dirs(path = "./Stock_Files") ) >= 1 ) {

stock_dir <- paste0(getwd(),"/Stock_Files")

stock_files <- list.files(path = stock_dir,

pattern = "csv$")

} else {

# Create a directory

dir.create("./Stock_Files",

showWarnings = TRUE,

recursive = FALSE,

mode = "0777")

# Create multiple temporary file names

stock_files <- tibble::tibble(

id = seq(1, val, 1),

file_path = seq(1, val, 1) %>%

map(~ tempfile(

pattern = paste0("temp_stock_",.x),

tmpdir = stock_dir,

fileext = ".csv"))

)

# Download the files using temporary directory and file names

for(i in seq_along(1:val)){

try(

download.file(download_links$link[i],

stock_files$file_path[[i]],

method = "wininet"),

silent = TRUE)

}

}We’ve successfully downloaded our files, but when we open some of them, we notice they’re empty!

It turns out only some of the files have information, those without information, are simply blank.

Interestingly, if we examine some of the empty files, we notice they’re only 3 bytes. We can use this to our advantage by deleting any file which has a size of 3 bytes or less.

# Record details on the files downloaded

detail_files <- fileSnapshot(stock_dir)

# Some months and thus files did not have any information, we make a list of those files

delete_files <- detail_files$info %>%

select(size) %>%

mutate(file = row.names(.),

file = paste0(stock_dir,"/",file)) %>%

filter(size <= 3 & str_detect(file, "csv$"))

# Delete all the unwanted files

invisible(

sapply(delete_files$file, unlink)

)

## Read in the remaining files

# Note files which are kept

kept_files <- detail_files$info %>%

select(size) %>%

mutate(file = row.names(.),

file = paste0(stock_dir,"/",file)) %>%

filter(size > 3 & str_detect(file, "csv$"))Now after this, we can at last read our kept files into memory.

# read in all the CSV files

data_raw <- map_dfr(.x = kept_files$file,

.f = read_csv,

skip = 1,

col_types = cols(

`Trade Date` = col_character(),

Security = col_character(),

Volume = col_character(),

High = col_character(),

Low = col_character(),

`Last Close` = col_character(),

`Current Close` = col_character(),

`Price Change` = col_character(),

`Bid Price` = col_character(),

`Ask Price` = col_character()

))Of the 1345 files downloaded, we deleted 0 and kept only 73.

Why so little? Well it so happens that the Stock Exchange only start recording information from around 2015, and we started our count from 1910, quite inefficient of us.

Well the reason we did this (notice I’m still using we), was to show how we can find ways to remove unneeded files without much issue. (That, and I was too lazy to manually check when useful information was recorded.)

Table showing Raw Data

# Show the first few values of the files we downloaded

data_raw %>%

head() %>%

gt::gt()| Trade Date | Security | Volume | High | Low | Last Close | Current Close | Price Change | Bid Price | Ask Price |

|---|---|---|---|---|---|---|---|---|---|

| 2015-01-01 | ABV | 1,500 | 0.32 | 0.32 | 0.00 | 0.32 | 0.00 | 0.25 | 0.30 |

| 2015-01-01 | BHL | 2,144 | 2.90 | 2.90 | 0.00 | 2.90 | 0.00 | 2.50 | 2.88 |

| 2015-01-01 | BCO | 13,899 | 1.90 | 1.65 | 0.00 | 1.82 | 0.00 | 1.90 | 0.00 |

| 2015-01-01 | CWBL | 11,900 | 3.00 | 3.00 | 0.00 | 3.00 | 0.00 | 0.00 | 2.48 |

| 2015-01-01 | CSP | 1,823 | 3.00 | 3.00 | 0.00 | 3.00 | 0.00 | 2.51 | 3.00 |

| 2015-01-01 | CPFD | 37,143 | 0.22 | 0.22 | 0.00 | 0.22 | 0.00 | 0.17 | 0.00 |

Cleaning Data

Well we have our data, but upon closer examination, we see it’s not in a format that’s particularly useful to us. At least not yet.

To hopefully make the cleaning process easier to follow, we’ll be using multiple temporary objects.

The first thing we will do is create two unique identifiers, they will track:

- the month and year for that particular row:

month-year - the particular row:

row_number

These values will prove useful later.

# Manipulate our raw data to include a unique identifier for month-year

d_raw <- data_raw %>%

mutate(month_year = clock::date_format(

clock::date_parse(`Trade Date`),

format = "%Y-%m"),

id = row_number())We also want to keep track of which row_number is the first value in a new month-year as well.

# Create a table which identifies the first index in the raw data for each month and year

id_val <- d_raw[

match(

unique(d_raw$month_year),

d_raw$month_year),] %>%

select(id)Now inside our Trade Date column, we sometimes get useful information which isn’t the date, but rather a title. We will now use our previous values to find their locations.

# Get the index numbers for each title

temp_row <- c(

which(

!str_detect(d_raw$`Trade Date`,

"([:digit:]|Trade Date)") | d_raw$id %in% id_val$id),

length(d_raw$`Trade Date`)

)We can now organize these temporary values into a usable table with which to use in our ‘cleaning’.

# Arrange index numbers into a usable format

temp_col <- tibble::tibble(

begin = temp_row[1:(length(temp_row)-1)],

end = temp_row[2:length(temp_row)],

Title = data_raw[begin,1][[1]]) %>%

mutate(Title = ifelse(str_detect(Title,

"[:digit:]"),

"BSE MAIN",

Title))Now using this table, we can at last carry out the last step of cleaning.

# Clean our data and assign to a new data frame

data_clean <- left_join(d_raw,

temp_col,

by = c("id"="begin")) %>%

# Fix NA values with a user made function, 'cleanNA'.

# You can find it at http://www.cookbook-r.com/

mutate(Title = cleanNA(Title),

`Trade Date` = clock::date_parse(`Trade Date`),

Volume = parse_number(Volume)) %>%

# Change valid columns from characters to numbers

mutate(across(High:`Ask Price`,

parse_number)) %>%

# Remove unneeded columns

select(-month_year:-end) %>%

# Remove rows with NAs

filter(complete.cases(.)) %>%

# Change valid columns from characters to factors

mutate(across(c(Security, Title),

as_factor))

min_rows <- min(data_clean$`Trade Date`)

max_rows <- max(data_clean$`Trade Date`)We’ve at last cleaned our data, which:

- Reduced our raw data table from 2413 rows to 2225

- Assigned the appropriate format appropriate for each column

- Moved all titles into a usable column

- Removed blank spaces and the like where applicable

Table showing Clean Data

data_clean %>%

head() %>%

gt::gt()| Trade Date | Security | Volume | High | Low | Last Close | Current Close | Price Change | Bid Price | Ask Price | Title |

|---|---|---|---|---|---|---|---|---|---|---|

| 2015-01-01 | ABV | 1500 | 0.32 | 0.32 | 0 | 0.32 | 0 | 0.25 | 0.30 | BSE MAIN |

| 2015-01-01 | BHL | 2144 | 2.90 | 2.90 | 0 | 2.90 | 0 | 2.50 | 2.88 | BSE MAIN |

| 2015-01-01 | BCO | 13899 | 1.90 | 1.65 | 0 | 1.82 | 0 | 1.90 | 0.00 | BSE MAIN |

| 2015-01-01 | CWBL | 11900 | 3.00 | 3.00 | 0 | 3.00 | 0 | 0.00 | 2.48 | BSE MAIN |

| 2015-01-01 | CSP | 1823 | 3.00 | 3.00 | 0 | 3.00 | 0 | 2.51 | 3.00 | BSE MAIN |

| 2015-01-01 | CPFD | 37143 | 0.22 | 0.22 | 0 | 0.22 | 0 | 0.17 | 0.00 | BSE MAIN |

We’ll remove some unneeded values before moving on.

# Remove unneeded variables

rm(data_raw,

delete_files,

detail_files,

download_links,

id_val,

kept_files,

temp_col,

base_link,

from,

to,

stock_dir,

stock_files,

val,

temp_row)Visualizing Data

Well we now have clean data, but what do we do with it?

As I mentioned before, I’m completely ignorant about stocks, so my guess is definitely not as good as yours.

Still we’ll move on undaunted, and plot something for now, we may explore this data properly at a later date.

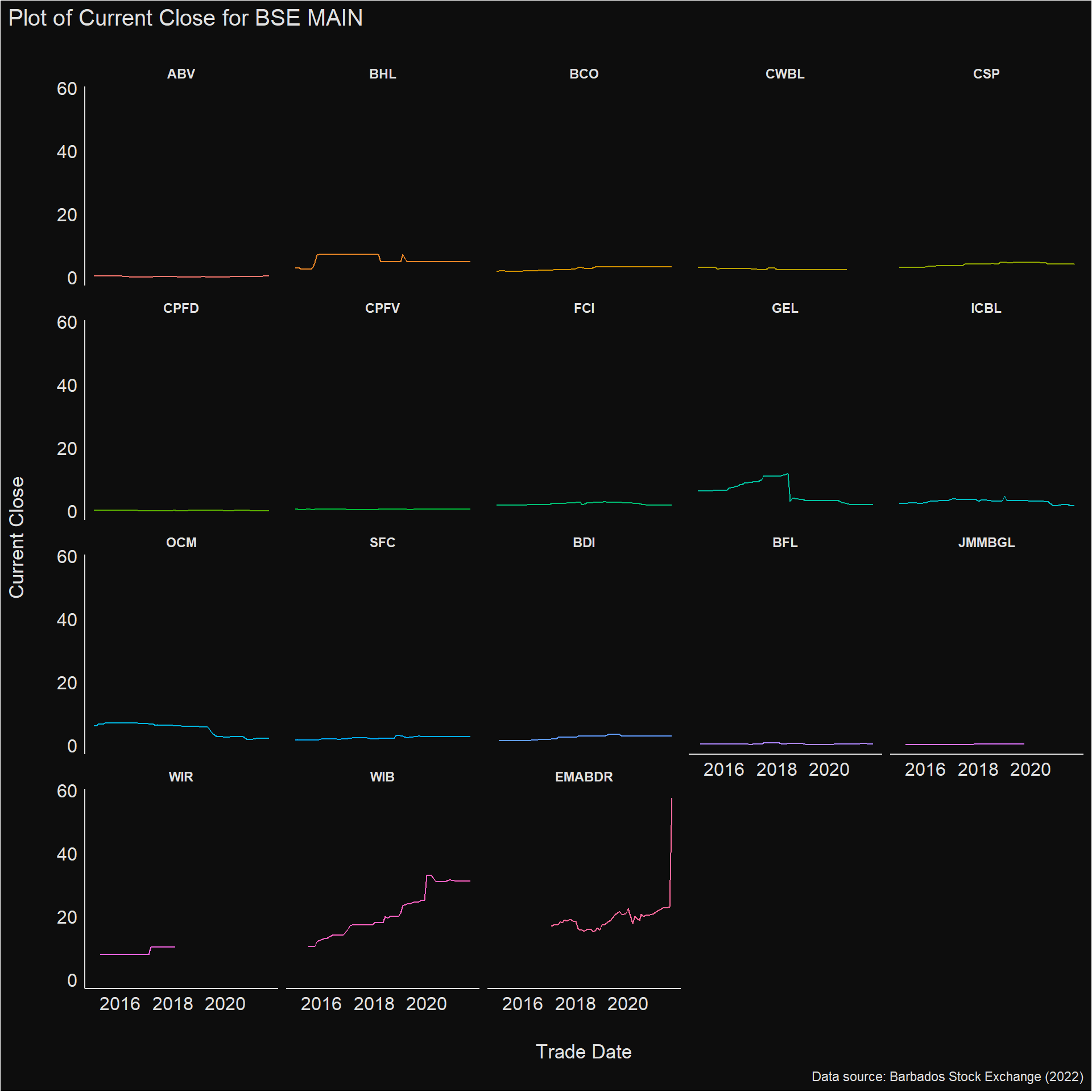

data_clean %>%

filter(Title == "BSE MAIN") %>%

ggplot(aes(x = `Trade Date`,

y = `Current Close`,

colour = Security)) +

geom_line(show.legend = FALSE) +

facet_wrap(vars(Security)) +

labs(title = "Plot of Current Close for BSE MAIN",

caption = "Data source: Barbados Stock Exchange (2022)") +

see::theme_blackboard() +

viridis::scale_fill_viridis()

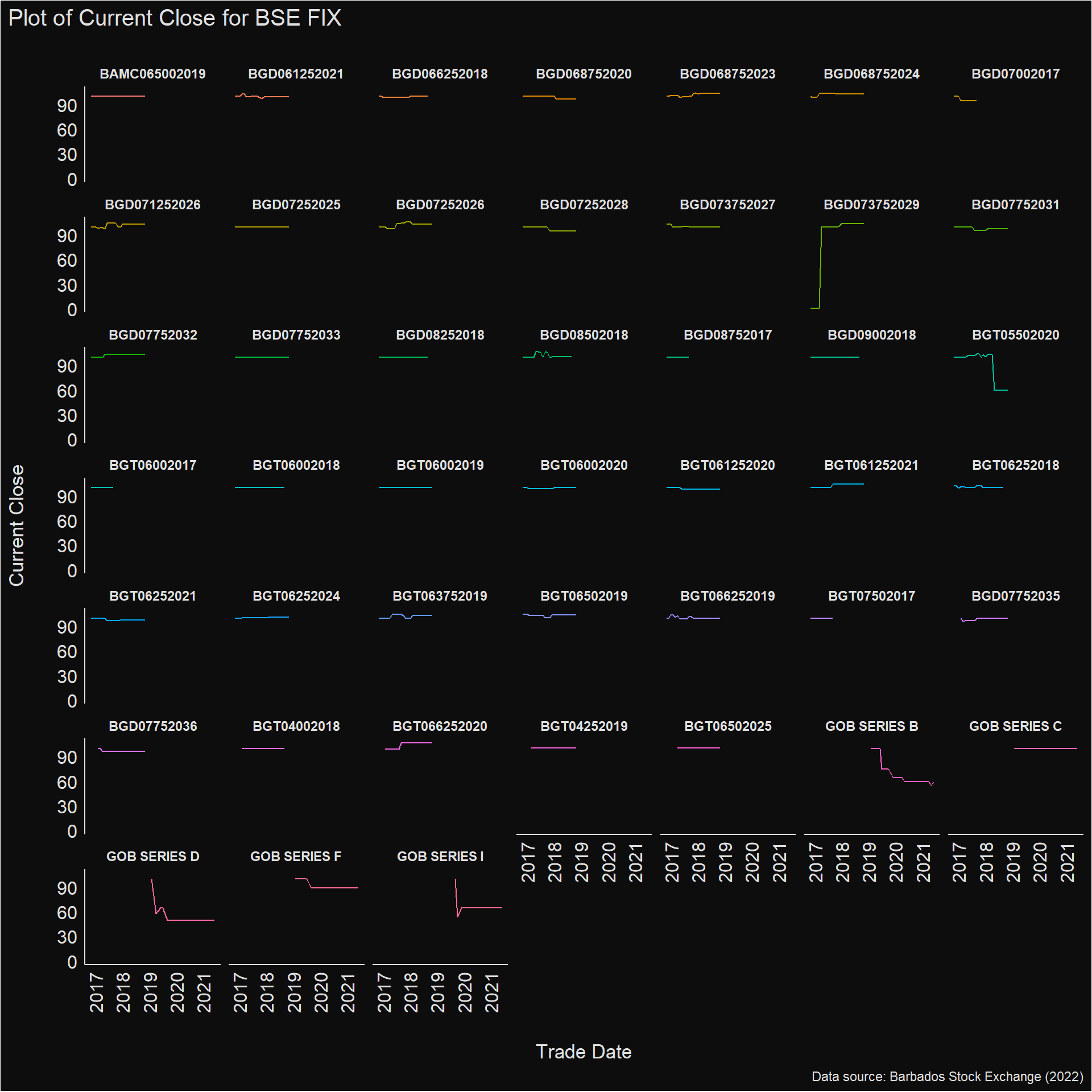

data_clean %>%

filter(Title == "Fixed Income") %>%

ggplot(aes(x = `Trade Date`,

y = `Current Close`,

colour = Security)) +

geom_line(show.legend = FALSE) +

facet_wrap(vars(Security)) +

labs(title = "Plot of Current Close for BSE FIX",

caption = "Data source: Barbados Stock Exchange (2022)") +

see::theme_blackboard() +

theme(axis.text.x = element_text(angle = 90)) +

viridis::scale_fill_viridis()

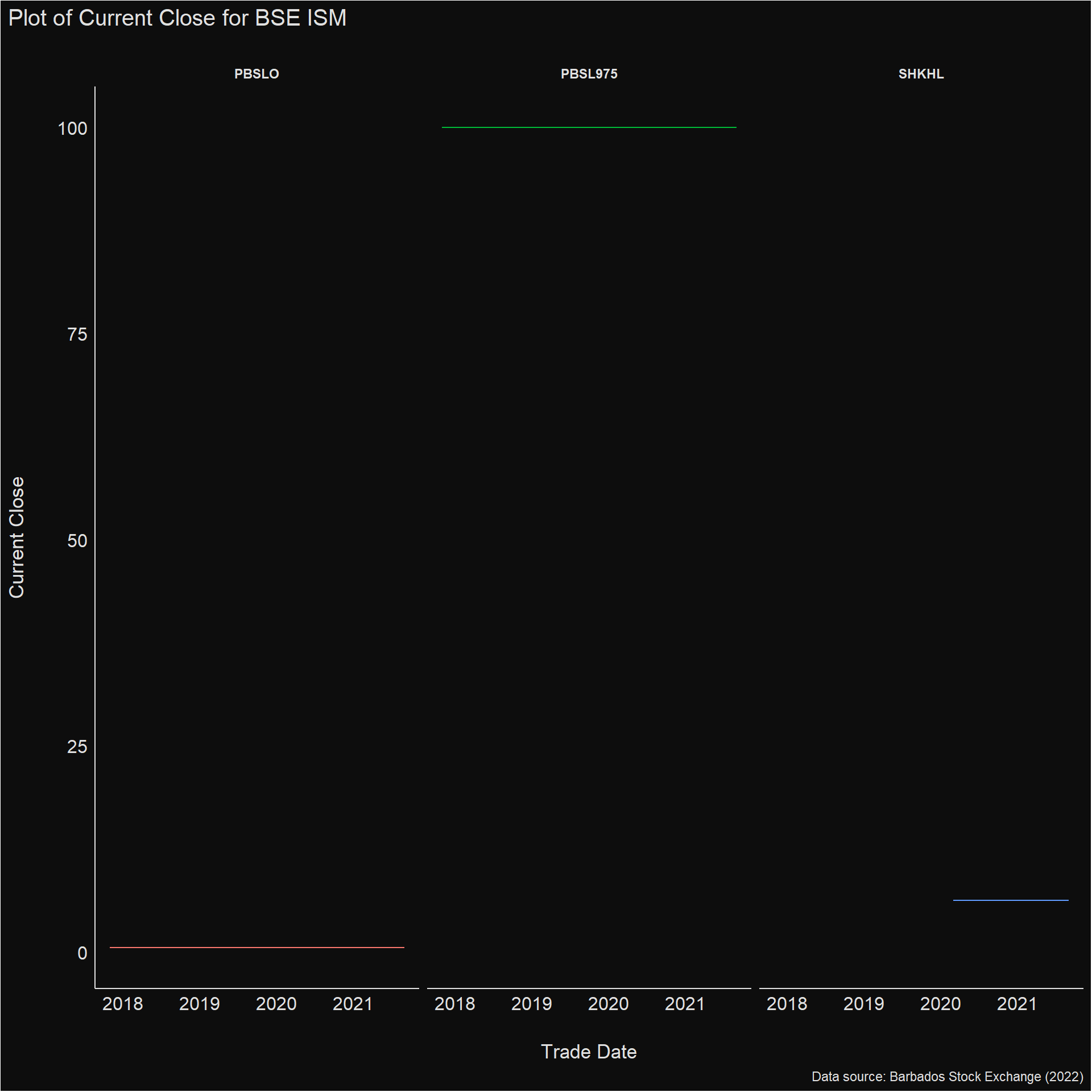

data_clean %>%

filter(Title == "ISM") %>%

ggplot(aes(x = `Trade Date`,

y = `Current Close`,

colour = Security)) +

geom_line(show.legend = FALSE) +

facet_wrap(vars(Security)) +

labs(title = "Plot of Current Close for BSE ISM",

caption = "Data source: Barbados Stock Exchange (2022)") +

see::theme_blackboard() +

viridis::scale_fill_viridis()

data_clean %>%

filter(Title == "BSE ISM-BONDS") %>%

ggplot(aes(x = `Trade Date`,

y = `Current Close`,

colour = Security)) +

geom_line(show.legend = FALSE) +

facet_wrap(vars(Security)) +

labs(title = "Plot of Current Close for BSE ISM-BONDS",

caption = "Data source: Barbados Stock Exchange (2022)") +

see::theme_blackboard() +

viridis::scale_fill_viridis()

This was a pretty interesting task.

If I revisit this, I’d like to confirm if BSE has an API of some form to use, and maybe I should learn a bit about stocks so I can do something interesting with the downloaded information.

Dario Clarke

Energy Analyst & Aspiring Data Analyst

My interests include sciences, religion and learning how people think.